Let us examine what happens when the clear and present danger from the coronavirus meets the global asset bubble, your portfolio and the industry standard investment approach. This is no small issue because – contrary to a market consensus – the coronavirus (COVID-19) is actually a real threat to complacent equity markets and client portfolios. It is a global health pandemic which requires active management in the real world, and which should also be risk managed by your adviser or super fund. The coronavirus and its real-world management should not simply be dismissed as just another flu, and could even be the catalyst which bursts the global asset bubble.

We will contrast two investment strategies and their approach to the coronavirus risk. The first investment approach is the one that you should all be familiar with because it is routinely used by nearly all advisers and super funds, and hence quite possibly one that is used by you. It is - of course - the “buy, hold and pretend we’re doing something” approach based on a passively managed strategic asset allocation (SAA). As we will explain, its response to risks such as the coronavirus is to pretend we’re watching it, do nothing of any substance with the portfolio, pretend that the portfolio is already diversified, and hope that it all goes away soon. This approach makes no substantive asset allocation changes and will never respond to a real-world event or risk in a sufficiently meaningful way.

The second investment approach is the road less travelled, even though you could be under the mistaken impression that this is what your adviser or super fund does (I don’t blame you for this understanding, as they may be telling you they do this, but in reality, only tinkering around the edges). It is an actively risk managed dynamic asset allocation approach (DAA), which is prepared to assess risks in real time and substantively change your portfolio weightings in accordance with a forward-looking view of risk and return. Its approach to the coronavirus is to actively research and consider the threat, and it is willing to actually change and de-risk your portfolio substantively as a result of this risk assessment.

Regardless of the outcome from this current risk to complacent asset pricing and advisers, we will demonstrate to you that the lack of management of the coronavirus risk by the routinely used industry standard SAA investment approach highlights the woefully poor client alignment and inadequate risk management of most advisers and super fund approaches. The SAA approach is based on convention, on a backward-looking consensus, and manages the career risk of the staff rather than clients’ risks. It is not focussed on protecting your capital from clear and present dangers, let alone other subtler threats. Effectively, I aim to demonstrate clearly and succinctly how the coronavirus highlights how the standard investment industry approach is flawed at managing money given a backward-looking view of the market environment, and won’t manage portfolio risks in the way you might reasonably expect it to, regardless of the danger. I will also explore how the truly client focussed adviser and investment approach is different and how your portfolio risk should be managed in your interest through an actively risk managed DAA approach.

To date, the coronavirus has been a non-issue for equity markets

Until now, the equity market has dismissed the issue as China-specific, containable and short-term in scope. (This is likely to change in short order as a complacent market wakes up to the risk.) Investors have superficially considered China to be successfully containing the threat given the official numbers show a decreasing trend of new cases, while global cases have been limited in scope and quite benign outside one exception; the (seemingly mismanaged quarantine of) the Diamond Princess cruise ship. A complacent and bullish market has simply compared the illness to historical outbreaks which have had little impact on markets, and hence dismissed it without much further thought or analysis. After all, who cares about coronavirus – or the real world - when central banks are busy pushing up asset prices and making the rich richer with easy money and low interest rates. The consensus wants to believe this time is different from prior cycles as current central banks and policy makers now seemingly control asset prices and seemingly want them kept high.

Substantial anecdotal evidence of supply chain issues and collapsing Chinese demand have hence been ignored or dismissed as temporary in scope, in a classic case of cognitive dissonance and wilful neglect. China is obviously one of the two most important economies in the world and any challenge to economic growth there should not be easily dismissed. Market signals from other asset classes (such as collapsing bond yields, commodity prices and soaring precious metals) have also been ignored, as has excessive positioning and bullishness within equities.

Indeed, since the coronavirus outbreak, equity markets have gone on to reach new highs, in response to continuing easy money and an increasing consensus extrapolation that interest rates can’t rise and will remain low forever, while conveniently believing growth will continue ad infinitum regardless. The former belief about low interest rates is understandable given high debt loads, government policy and various other economic factors, but still complacent given the woeful ineptitude historically of the market and central banks in picking the direction of interest rates beyond the short term. In a world with low real productivity requiring massive stimulus to grow even modestly, the latter belief about continuing growth ad infinitum in the face of substantive risks and unsustainable policy settings is foolish and inept.

So, what has your typical adviser or super fund done in the face of the threat?

Probably absolutely nothing. At best, they’ve tinkered. As they always do and always will do with an SAA approach.

Firstly, they do not perceive and have not done enough work to identify any substantive threat in the first place. They don’t perform much in the way of deep investigation themselves (that’d be difficult, and not that relevant if you aren’t going to do anything about it anyway). They have neither the interest or the capability to manage a substantive tail risk like this. They don’t even think the market is in a bubble currently, conveniently ignoring the massive global central bank stimulus required to keep this market up, and the huge fiscal deficits in the US and elsewhere required to produce miniscule rates of fake growth.

Secondly, even if they perceived there was a threat, what would they do about it? Not much.Their investment approach is built around managing to a strategic benchmark and is always going to be heavily invested and reliant on equities. They are most afraid of being different, and indeed lack the courage to be substantively different from peers or consensus. They like to pretend there is no alternative to equities. The risk they’re managing to is their own career risk and the risk that they’re different and wrong. Being the same and losing money for clients is not as big an issue, at least for them; if the market falls, they can simply say “The market will bounce back”, or “Who could have seen that coming!” or “We outperformed by 2% (as the market lost 50%)”. They may not know much or anything about other asset class options, managing portfolios holistically, and very little about alternatives and true active management. Choosing alternative or active managers is too much hard work and too difficult, requiring skills that they don’t have, don’t want to learn and don’t want to pay for when they can clip the ticket more easily and sell a consensus. Their investment approach works for them; the workload is low, the profits are good, and the demands are light.

The important point to realise here is that the typical and conventional SAA approach is always going to be heavily invested in long only equities and very passive by nature, no matter what happens. It never sells to any substantive degree, is relatively aggressive in its risk tolerance, and is hence well-suited to a bull market, while being destructive in a bear market or crisis. It will ride the cycle up or down; making money with stocks when they go up, and collapsing with them when markets fall. Sadly, chances are that this is your investment adviser or superannuation or retirement fund. You’re probably not special and they’re probably not different. However, and most importantly, this approach is not actually aligned with what you as a client probably want, need or expect.

What would a truly client focussed approach be doing instead?

The investment approach you probably want and deserve is actually managing your portfolio in a way which is aligned with your goals. Importantly, that involves managing the big risks to your money, not just providing a return that rides the equity market up, and then down. You might personally recognise that the equity markets are in a bubble driven by low cash rates and policy manipulation, and is overly complacent, if not delusional. You may hence consider it necessary to invest with someone who also knows this and is prepared to invest your portfolio accordingly and more prudently by avoiding excessive risk and overpriced assets. You can’t afford another GFC and you know experiencing big losses is intolerable and unacceptable, as it destroys long term compounding and returns. You don’t want your retirement prospects to collapse merely because the equity or bond market does and your adviser or super fund is managing their own risks ahead of yours.

The truly active risk manager is laser focussed on the risks to asset values and prices. They are already running much better diversified portfolios than simply being invested in plain vanilla equities, bonds and (still interest rates sensitive) variations of these such as private equities, property and debt. Instead, they have substantive exposure to skilfully chosen alternatives and genuine active management. They have you invested in a genuine multi-asset portfolio that is actively managed and selected based on its expected resilience to known risks and clear and present dangers. It will typically, for example, have a meaningful allocation to precious metals because of their “crisis hedge” attributes and competitive return prospects. Your manager can show you that your portfolio is genuinely different (e.g. it holds long short and market neutral alternatives, precious metals, and the portfolio weightings are actively changed), and that your portfolio produces lowly correlated and differentiated results to others (because it is managed to your goals, rather than to consensus expectations).

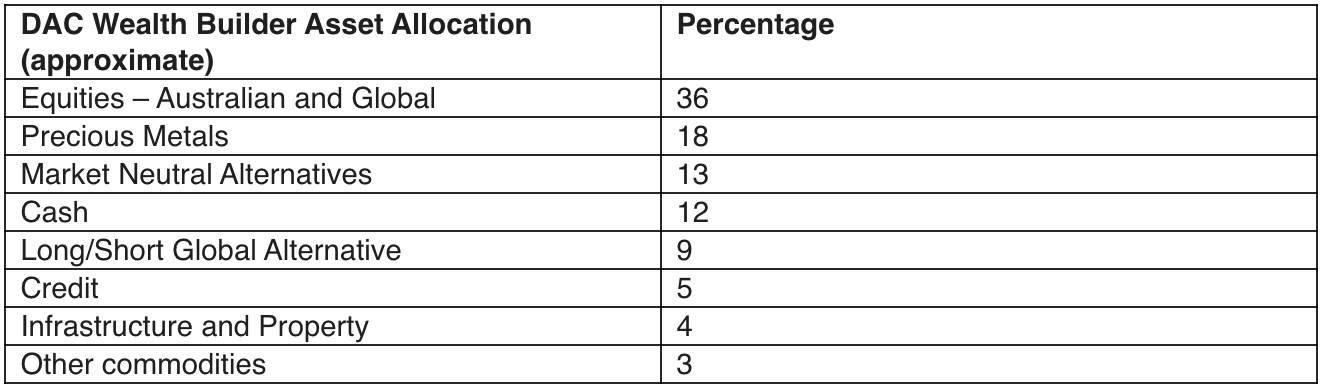

The below is a recent weighting from Dynamic Asset’s Wealth Builder Portfolio, which has a growth objective like your average super fund or adviser and is daily liquid. You will notice substantially lower equity risk allocations and more diverse holdings than the industry standard growth or super fund (which would have around 70% in long only equities, property and infrastructure (versus just 40%). There is much greater use of skilled alternatives including market neutral, long short and precious metals. In addition, the allocations actually move around substantially more through time.

Interestingly, the current weightings are actually quite similar to that of an endowment fund such as the Future Fund, albeit without the same use of illiquid assets. Returns last year were also very similar to that of the Future Fund. No loss has been experienced this month as of COB on the 25th February with minor losses expected by the end of the month, massively above the average growth fund.

Table: Sample dynamic asset allocation

Lucerne’s Alternative Investment Fund (circa 90% Alternatives, 10% Cash) is massively different from the typical growth fund. It is also diversified, albeit by using highly complementary strategies which are actively and skilfully managed in size to reduce risk prospectively. It has very high use of highly skilled alternative managers with low market dependency and high active risk and added value. It bears no resemblance to typical growth funds whatsoever, yet targets similar return prospects long term with a smoother ride and much lower drawdown expectations (minor drawdowns only experienced thus far, including none expected for this month).

(Ed's note: please read the relevant disclosures at the bottom of this article)

The active DAA approach can demonstrate that they change what they do in response to market conditions and prospects because they prioritise the return of your capital as much as the return on your capital. They recognise that this requires real skill and aptitude and hence have the personnel expertise required to successfully manage a DAA approach. They’re not paying their corporate bureaucrats and managers a small fortune to parrot consensus, or provide something an armchair investor can do themselves with little effort. Importantly, your adviser can convincingly explain why your portfolio won’t collapse when the bond or equity bubble ends...

Furthermore, your manager actually knows a lot about coronavirus because they have actually researched it. They recognise it is a potential threat to your wellbeing and your portfolio. They have real insight and knowledge of the subject matter and have assessed the risk rather than dismissed it. They recognise the coronavirus risk as growing and have moved to protect your capital, or already have low risk of large capital losses due to their genuine and extensive diversification away from expensive assets. They have compared the market’s complacency to what is happening on the ground, and know that consumption and supply chains are being dramatically affected. They recognise that the Chinese economy has ground to a halt and that it will be difficult to get the Chinese successfully back to work quickly without flare-ups of the virus causing further substantive health and economic challenges. They can see that other countries are going to have to respond with their own escalating containment measures and that this will affect growth prospects and economic and investment confidence. They are interested in real world profits, and are not just extrapolating market momentum and parroting market consensus. They know that if economies enter recession due to the impacts from the containment measures, then the extended late market cycle is probably over as credit spreads widen and continuing buy-backs become improbable. If growth is suddenly not continuing ad infinitum, then the consensus “goldilocks” bull market thesis suddenly becomes highly challenged almost irrespective of central bank action. Sadly, this cycle probably eventually ends like every other, and the delusions that central planning will be more successful this time will once again be proven fallible. This is an entirely predictable outcome.

What can we learn from this?

It may be a surprise to some, but in the real world the client focussed DAA risk manager and adviser we highlight above is truly hard to find. They are the exception and not the rule. Their job is a more difficult one compared to pretending that everything will be ok no matter what is happening today, or that the equity market is always efficient and always worth buying and holding, which is balderdash. It takes tremendous courage (and hard-work) to be different and to do so successfully and thoughtfully, so obviously, this is a role that few are suitable for. But most importantly, some are prepared to be different and do the work in your interest, and this offers clients a substantive choice and alternative, where there is otherwise simply pretence...

As mentioned, the above non-consensus assessment of the coronavirus has been dismissed by equity markets and by most adviser and super funds – who simply don’t care enough to perform this depth of risk assessment themselves. Importantly, the coronavirus should never have been dismissed so easily by most and by the market (even weeks ago) given the high infectivity, the response by the Chinese government, the early assessment by industry experts, and the apparent attributes of the virus. Indeed, I wrote on 29th January (nearly a month ago now) that “the equity market really appears to be dismissing the risk related to this issue and the potential requirement for greater mitigation. This seems strange given the characteristics of the virus have not been fully identified and hence there is a real risk this could get a lot worse and become a big problem globally, and not just for China and Chinese growth. It is unclear for instance currently whether transmission can occur while someone is asymptomatic, and for how long this might be the case.” Since then, the Chinese have taken dramatic steps to attempt containment of the risk, their economic activity has collapsed, and global asymptomatic transmission is occurring as we write as the latency period is extended. Indeed, in the last few days, we have seen an explosion of cases in Korea, Italy and Iran and more than 30 countries globally have discovered and experienced coronavirus, including many which seemingly involve local transmission of the virus. The World Health Organisation and other industry experts have implied and support our assertion that containment may now be difficult, if not impossible, which has dramatic implications.

We have hence shown that most advisors and super funds have demonstrated complacency, mediocrity and lack of prudent portfolio risk management, regardless of what transpires from here (they rely on luck rather than good management!). It is important to realise that regardless of how risky the market becomes, the SAA portfolio doesn’t change meaningfully from one year to the next and is very similar in positioning to everyone else’s portfolios with similar “risk profiles”. The portfolios are in reality determined by peers, historical convention and market consensus. This contrasts with what the goals, needs and expectations of clients usually are and what would best manage the risks to portfolios as investment risks and market valuations change through time. Instead, the SAA approach is heavily dependent on the bull market in bonds and equities continuing. It doesn’t include meaningful diversification from large allocations to genuine interest rate insensitive alternatives, active management or precious metals. In contrast, the actively risk managed DAA approach can offer a genuinely diversified and risk-controlled approach through time, and in so doing better aligns with the absolute return and risk preferences and needs of most investors. It can actually manage end of cycle portfolio risks. You might need that right now! In any case, greater diversification and avoidance of concentrated portfolio risks is crucial if you recognise the future as uncertain, regardless of the eventual outcome.

So what can you do?

If you want your money truly risk managed in accordance with your goals and expectations, ascertain whether the adviser, super fund and investment approach you are using is best suited to doing this. Is there a better way to protect and grow your money? A strategic asset allocation approach is poorly suited for the current market environment, stage of the cycle and current market risks, including the imminent threats from the coronavirus. The SAA approach is based on convention rather than excellence. It is not forward-looking and highly ineffective in crises and bear markets, in contrast to a well-managed risk managed DAA approach which is ready for these today. Regardless of whether equity markets fall imminently (which we assess as becoming increasingly likely), the risks being taken with your money by an SAA approach and its likely return profile and downside may be unacceptable to you, as it is to me. This may hence prove a perfect time to switch. If you have been lucky enough to have made a fortune in the huge long bull market we’ve already experienced, you can cash in your profits rather than watch them disappear when the cycle ends. Luck doesn’t typically last while prudent management persists. By reducing risk and moving to a more risk-managed and genuinely diversified approach today, you will effectively lock in and realise the paper gains you’re dangerous sitting on, and greatly reduce the risk of seeing these disappear in the coming crisis and bear market. I promised you a call to action to stop you being “coronered”, and I meant it. You don’t need to be “coronered”, whether now or shortly, so don’t be. There is a better way.

This article was originally seen in Livewire

Find out more about Dynamic Asset's Adviser Investment approach.

RELATED CONTENT